Getting Started with Insurance: The Absolute Basics You Need to Know

Getting Started with Insurance: The Absolute Basics You Need to Know (2025 Edition)

If you’ve opened an insurance renewal envelope recently and felt your stomach drop, you aren’t alone. In my 15 years analyzing financial markets, I’ve never seen a “Hard Market” quite like this one.

Here is the brutal truth: Insurance is no longer just paperwork you file away and forget. In an era of persistent inflation and rising climate risks, insurance has become the primary defensive wall between you and financial ruin. Yet, most beginner guides are still defining terms like it’s 2010.

You don’t just need definitions; you need a survival strategy. This comprehensive guide will walk you through the absolute basics of insurance, explain why you are paying so much in 2025, and provide actionable ways to structure your “wealth defense” without going broke.

Table of Contents

- What is Insurance, Actually? (Risk Transfer 101)

- The “Hard Market”: Why 2025 Prices Are So High

- The “Big 4” Types of Insurance You Need

- Auto Insurance: Navigating the 11% Hike

- Home & Renters: The Inflation Trap

- Health Insurance: Decoding the Alphabet Soup

- Life Insurance: The Coverage Gap

- Strategic Buying: How to Save in a Hard Market

What is Insurance, Actually? (Risk Transfer 101)

Before we talk about policies, we need to talk about risk. Life is inherently risky. You could crash your car, your apartment could catch fire, or you could fall ill. In finance, you have two choices regarding these risks:

- Self-Insure: You save enough cash to pay for a new car or heart surgery out of pocket (Risk Retention).

- Transfer Risk: You pay a fee to a third party to take that risk for you (Risk Transfer).

Insurance is simply the mechanism of risk transfer. You pay a small, known amount (premium) to avoid a potentially catastrophic, unknown amount (a claim). It operates on the “Law of Large Numbers”—insurers pool money from thousands of people, knowing only a few will need a payout in any given year.

The Key Terminology Glossary

To survive the 2025 market, you must understand the “Big Three” terms that determine your financial exposure:

- Premium: The subscription fee you pay (monthly or annually) to keep the policy active.

- Deductible: Your “skin in the game.” This is the amount you must pay before the insurance company pays a dime. Generally, a higher deductible equals a lower premium.

- Limit of Liability: The maximum amount the insurer will pay. If you have a $50,000 limit and cause $80,000 in damages, you are personally sued for the remaining $30,000.

The “Hard Market”: Why 2025 Prices Are So High

If you are wondering, “Why did my rate go up if I didn’t make a claim?”, you are a victim of what industry experts call a Hard Market.

In a hard market, insurance carriers tighten their underwriting standards and raise premiums across the board. This isn’t random; it’s driven by three massive economic forces:

- Social Inflation: This is a massive driver in 2024-2025. According to the Swiss Re Social Inflation Index 2024, rising litigation costs have increased U.S. liability claims by 57% over the past decade. Put simply: lawsuits are getting more expensive, and juries are awarding bigger payouts.

- Climate Risk: From wildfires in the West to hurricanes in Florida, weather events are becoming more frequent and severe. Swiss Re’s Sigma Report forecasts global premiums will grow 2.6% annually through 2026 largely to cover these catastrophic losses.

- Tech Inflation: A fender bender in 2010 meant replacing a plastic bumper. In 2025, that bumper is filled with sensors, cameras, and LIDAR. Repair costs have skyrocketed, driving up premiums.

The “Big 4” Types of Insurance You Need

While there is insurance for everything (even alien abduction), there are four pillars that form the foundation of a secure financial life. Skipping any of these exposes you to ruin.

1. Auto Insurance: Navigating the 11% Hike

Auto insurance is mandatory in almost every state, but relying on the state minimum is a rookie mistake. With the average cost of a new car exceeding $48,000, state minimums (often as low as $15,000 or $25,000 for property damage) are woefully inadequate.

The 2025 Strategy: Usage-Based Insurance (UBI)

If you are a safe driver, you are currently subsidizing bad drivers. Traffic violations actually increased 17% in 2024, according to LexisNexis Risk Solutions. To break away from the pack, consider UBI (telematics). This involves letting the insurer track your driving via an app. It is the single most effective way to lower premiums in the current market.

2. Homeowners & Renters Insurance: The Inflation Trap

Whether you own or rent, your biggest risk in 2025 is Underinsurance.

For Homeowners:

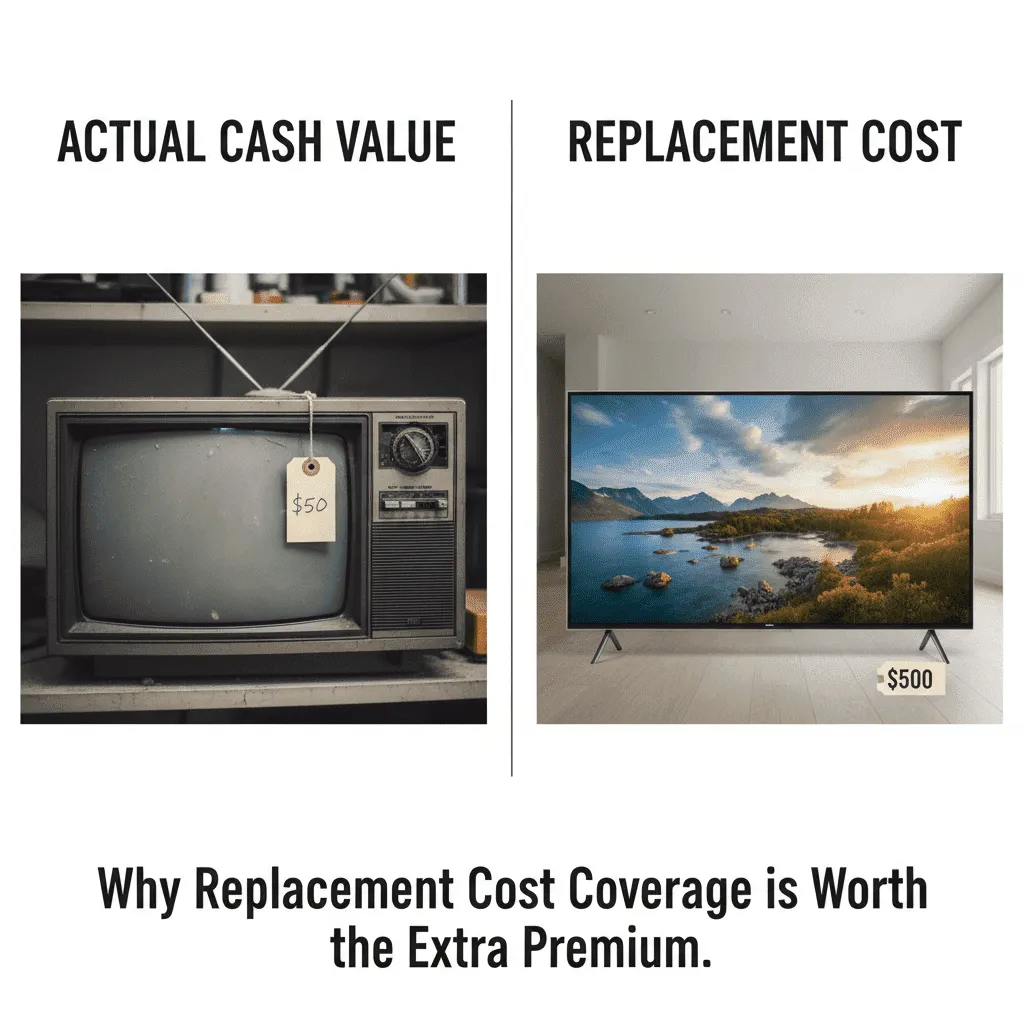

The cost to build a home has risen faster than general inflation. If you haven’t updated your policy limits since 2022, you might only be covered for 80% of your home’s rebuilding cost. Always insure for Replacement Cost, not Market Value.

For Renters:

I am constantly surprised by how many young professionals skip this. According to NerdWallet’s 2024 analysis, the average renters insurance policy costs just $148 per year (about $12/month). It covers your laptop, clothes, and furniture if your apartment burns down, but more importantly, it provides liability coverage if you accidentally injure someone or damage their property.

3. Health Insurance: Decoding the Alphabet Soup

With family premiums topping $25,000 (per KFF data), choosing the right plan is critical. The main choice usually comes down to HMO vs. PPO:

- HMO (Health Maintenance Organization): Generally cheaper premiums, but you must use their network of doctors and usually need a referral to see a specialist.

- PPO (Preferred Provider Organization): Higher premiums and deductibles, but you have the freedom to see any doctor without a referral, including out-of-network providers (at a higher cost).

The HSA Advantage: If you are young and healthy, consider a High Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA). This is the only “triple-tax-advantaged” account in the U.S. tax code, acting as a super-charged retirement vehicle for healthcare costs.

4. Life Insurance: The Coverage Gap

According to the LIMRA 2024 Insurance Barometer Study, there is a record-high need gap: 102 million Americans know they need more life insurance but haven’t bought it.

Term vs. Whole Life: The Verdict

For 95% of people reading this, Term Life Insurance is the correct choice. It functions like auto insurance—you pay for coverage for a set period (e.g., 20 years) to protect your children while they are young. Whole Life insurance mixes insurance with an investment component, often resulting in high fees and mediocre returns compared to the stock market.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Cost | Very Affordable ($20-$40/mo) | Expensive (5x-10x cost of Term) |

| Duration | Specific period (10-30 years) | Lifetime (as long as premiums are paid) |

| Cash Value | None (Pure protection) | Builds cash value over time |

| Best For | Parents, Homeowners, Income Replacement | Estate Planning for Ultra-Wealthy |

Interactive Tool: The Deductible Strategy

One of the easiest ways to lower your premium is to raise your deductible. But is it worth the risk? Use this simple calculator to see how long you need to go claim-free to break even.

Deductible Savings Calculator

Strategic Buying: How to Save in a Hard Market

Navigating the insurance landscape in 2025 requires active management. Loyalty doesn’t pay; insurers often use “price optimization” algorithms that slowly raise rates on loyal customers who don’t shop around.

1. The Credit Score Impact

In most states (excluding CA, HI, MA, and MI), your credit-based insurance score is a massive factor in your premium. Data indicates that drivers with poor credit can pay nearly double what drivers with excellent credit pay for the exact same coverage. Improving your credit score is effectively an insurance discount.

2. The Bundle

Bundling home and auto insurance is the oldest trick in the book because it works. Insurers like State Farm, Allstate, and Progressive typically offer discounts ranging from 10% to 25% for bundling. In a hard market, this stackable discount is essential.

3. The Annual Review

Set a calendar reminder. Every 12 months, shop your policy. Even if you don’t switch, having a lower quote from a competitor gives you leverage to call your current agent and ask for a policy review.

Frequently Asked Questions (FAQ)

Is insurance worth it if I never file a claim?

Yes. You aren’t paying for the payout; you are paying for the transfer of risk. The “peace of mind” value—knowing that a lawsuit or fire won’t bankrupt you—is the product. Furthermore, for auto and health, it is a legal or practical necessity.

What happens if I stop paying my insurance premium?

Your coverage will lapse. If you have a lapse in auto insurance coverage, insurers view you as “high risk” when you try to buy a policy again, leading to significantly higher premiums (sometimes 30-50% higher) for the first 6 months of a new policy.

Can I negotiate my insurance rates?

Not directly. Insurance rates are filed with state regulators and cannot be arbitrarily changed by an agent. However, you can negotiate by adjusting coverages, raising deductibles, or finding discounts you qualify for but aren’t receiving.

Conclusion: Your Declaration Page is Your Defense

We are living through a historic shift in the insurance industry. The “Hard Market” of 2024-2025 means that wealth protection costs more than it used to. But as Bankrate’s 2025 data shows, the cost of not having insurance—or having the wrong insurance—is rising even faster.

Your Action Plan for Today:

- Dig out your “Declaration Page” (the first page of your policy).

- Check your Liability Limits—are they high enough to protect your current assets?

- Check your Deductible—can you afford to raise it to $1,000 to save on monthly premiums?

- If you rent, buy a policy immediately.

Don’t view insurance as a tax on your existence. View it as the moat around your financial castle. In an unpredictable economy, it’s the one thing that keeps your future secure.