Raise Your Deductible or Keep It Low? Understanding the Cost Trade-offs

Raise Your Deductible or Keep It Low? Understanding the Cost Trade-offs in 2025

A definitive guide to navigating inflation, break-even analysis, and financial risk.

I recently opened my auto insurance renewal letter, and my jaw hit the floor. Despite a clean driving record and zero claims, my premium had jumped significantly. If you’re reading this, you’ve likely experienced the same shock. You aren’t alone.

In 2025, insurance premiums have hit record highs. According to a July 2025 report from ValuePenguin / Insurance Information Institute, auto insurance premiums are expected to rise an average of 7.5% this year, following a massive 15% jump in previous cycles. Homeowners aren’t faring any better; the Insurance Information Institute (III) noted in May 2025 that the average homeowners insurance premium rose by 11.2% year-over-year.

Faced with these rising fixed costs, the fastest lever you can pull to lower your monthly bill is raising your deductible. But is the immediate cash flow worth the risk of a massive out-of-pocket expense later?

This isn’t just a guessing game. It’s a math problem. In this guide, we move beyond “it depends” and provide the mathematical “Rule of Break-Even” to help you decide if you should raise your deductible or keep it low.

- The “Seesaw Effect” of premiums vs. deductibles.

- How to calculate your exact break-even point (Calculator included).

- Why $1,000 is becoming the new standard for auto insurance.

- The “Mega-Deductible” trend in home insurance.

- The critical “Sleep at Night” factor involving your emergency fund.

The Core Trade-off: Premium vs. Deductible Explained

To make a smart decision, we have to strip insurance down to its basics. Insurance is essentially risk transfer. You are paying a company to take on risk that you cannot afford to handle yourself.

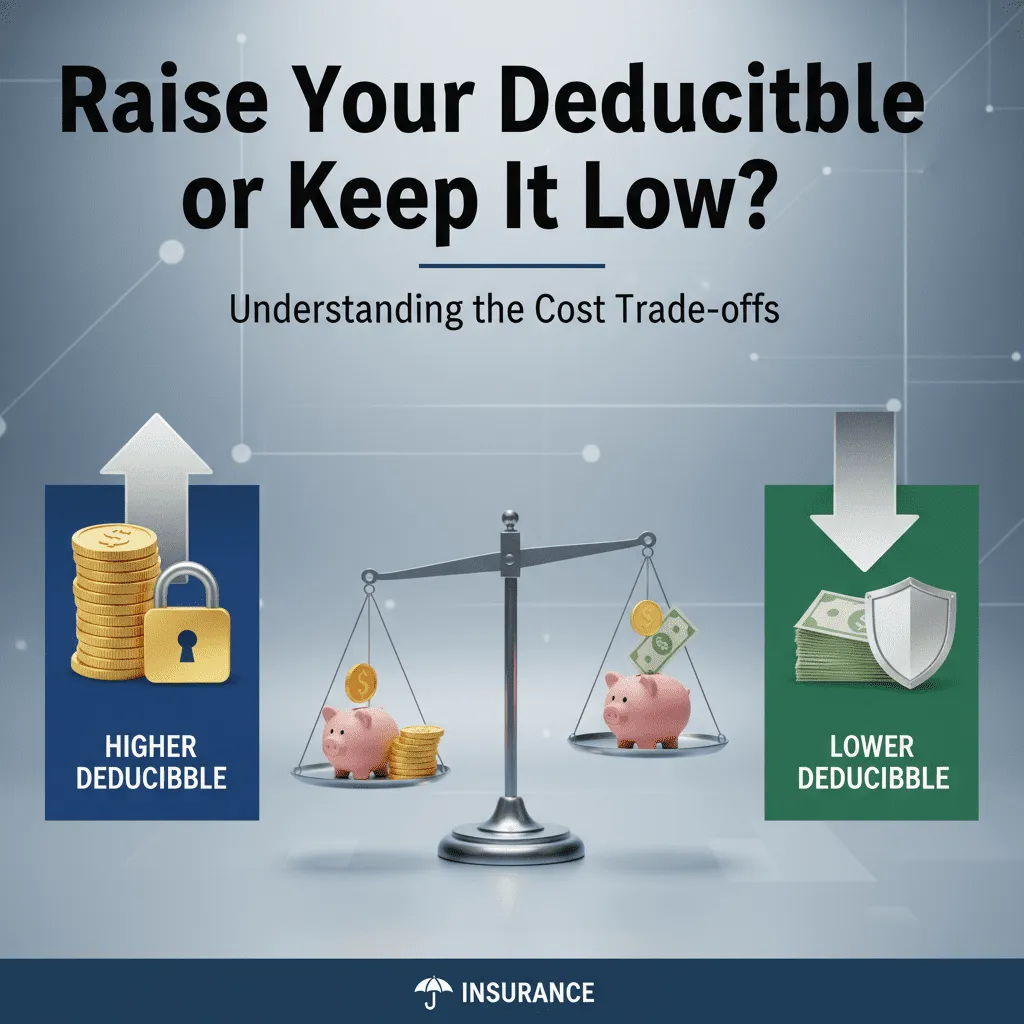

The Inverse Relationship (The Seesaw Effect)

Think of your insurance policy as a seesaw. On one side, you have your Premium (the fixed amount you pay every month or year). On the other side is your Deductible (the amount you must pay out-of-pocket before the insurance company pays a dime).

When you raise the deductible side of the seesaw, the premium side goes down. Conversely, if you want a low deductible (meaning the insurer takes more risk), your premium must go up.

In my years of analyzing financial products, I’ve found that people often view the premium as a “loss” and the deductible as a “threat.” But in 2025, the math is shifting. Because repair costs have skyrocketed due to inflation, insurers are charging a premium—literally—for low deductibles.

“Fixed Cost” vs. “Contingent Cost”

Here is the reality check: Your premium is a guaranteed loss. You will pay that money whether you crash your car or not. Your deductible is a contingent cost. You only pay it if something bad happens.

The strategic question is: How much guaranteed money are you willing to lose to avoid a potential cost that might never happen?

— Breanne Armstrong, Director of Global Insurance Intelligence at J.D. Power (June 2025)

The Math: When Does Raising Your Deductible Make Sense?

Emotions shouldn’t dictate your financial security. Numbers should. To determine if raising your deductible is a smart move, you need to calculate the Break-Even Period. This is the amount of time you need to go claim-free for the premium savings to equal the extra risk you are taking on.

The Break-Even Calculation (The “3-Year Rule”)

General financial wisdom suggests that if your break-even period is under three years, raising your deductible is usually a statistically sound decision. If it takes 10 years to break even, the risk is likely too high compared to the reward.

The Formula:

(Difference in Deductible Coverage) ÷ (Annual Premium Savings) = Years to Break Even

Interactive Break-Even Calculator

Enter your numbers below to see if raising your deductible makes sense.

Case Study: The “Safe Driver” Switch

Let’s look at a real-world scenario from Ohio based on 2025 rate structures.

- Scenario: A driver switches their Auto Deductible from $250 to $1,000.

- Savings: Their premium drops from $1,400/year to $1,150/year (Saving $250 annually).

- Risk: They are taking on an additional $750 of potential cost ($1,000 – $250).

- Calculation: $750 Risk ÷ $250 Savings = 3 Years.

Verdict: This is a smart move. Why? Because statistically, the average driver files a collision claim only once every 17.9 years. Betting that you can go 3 years without an accident is a wager the odds favor heavily.

Auto Insurance: The $1,000 Standard

For decades, $500 was the “standard” deductible. In 2025, that advice is outdated. Inflation has pushed repair costs so high that insurers are punishing low deductibles with disproportionately high premiums.

Why $500 is No Longer the “Smart” Default

According to J.D. Power’s “2025 U.S. Auto Claims Satisfaction Study” (October 2025), 26% of auto insurance customers now carry deductibles of $1,000 or more. This migration is driven by necessity. With the national average cost for full coverage car insurance hitting $2,424 per year (according to Bankrate’s 2025 True Cost of Auto Insurance Report), consumers are desperate for relief.

I recently spoke with a client who was hesitant to raise her deductible. I asked her, “If you had a $600 fender bender, would you file a claim?” She said no, fearing her rates would go up. If you wouldn’t file a claim for $600, why are you paying extra for a $500 deductible? You are paying for coverage you are afraid to use.

7% of auto insurance customers avoided filing a claim in 2025 specifically because they feared their rates would rise, according to J.D. Power data. If you are in this group, a higher deductible is a logical step.

Inflation’s Impact on Claims

Why are premiums rising? Cars are smarter, but they are more fragile. Sherif Gemayel, CEO of Trufla, noted in May 2025: “Replacing a windshield is not just a windshield anymore. A windshield in a new car might have cameras or sensors integrated… driving up the cost of claims and premiums.”

By raising your deductible to $1,000, you are essentially telling the insurer, “I will handle the minor bumps and scratches; you handle the total losses.” This aligns better with the modern reality of repair costs.

Homeowners Insurance: The Percentage Trap

While auto insurance claims are somewhat frequent, homeowners insurance is a different beast. The stakes are higher, but the frequency is lower. This changes the calculus significantly.

Claim Frequency Stats: The 10-Year Reality

According to the Insurance Information Institute, the average homeowner only files a claim once every 9 to 10 years. This low frequency suggests that homeowners insurance should primarily be treated as catastrophic coverage.

Based on Kiplinger’s January 2025 data, boosting a home deductible to $2,500 can save roughly 24%, and raising it to $5,000 can save upwards of 37%. Over a 10-year period (the average time between claims), those savings can amount to thousands of dollars—far exceeding the deductible difference.

The “Mega-Deductible” Trend

We are seeing a surge in what I call “Mega-Deductibles.” A March 2024 Market Report by Guaranteed Rate Insurance noted that deductibles in the $5,000 to $10,000 range saw a 49% increase in adoption. Homeowners are realizing that filing a small claim (e.g., $1,500 for a water leak) is often a mistake that leads to higher premiums or non-renewal.

— Jeanne Salvatore, Chief Communication Officer at Insurance Information Institute

Wind, Hail, and The Percentage Trap

A critical warning for 2025: Check your policy for “Percentage Deductibles.” In high-risk states like Colorado, Texas, and Florida, insurers are shifting from flat-rate deductibles (e.g., $1,000) to percentage-based deductibles (e.g., 2% of the home’s insured value).

If your home is insured for $500,000, a 2% wind/hail deductible means you are on the hook for $10,000 before insurance kicks in. In this case, you don’t have a choice to “keep it low”—the market has raised it for you. You must ensure your emergency fund matches this new liability.

Health Insurance (HDHP): A Different Beast

When we talk about raising deductibles in health insurance, we are usually discussing High Deductible Health Plans (HDHPs). This isn’t just about saving on premiums; it’s about tax strategy.

The HSA Advantage

According to the Kaiser Family Foundation (KFF) 2024 Employer Health Benefits Survey, the average annual deductible for single coverage was $1,787. For small business employees, that jumps to $2,575.

The primary reason to choose a high deductible here is access to a Health Savings Account (HSA). An HSA is a triple-tax-advantaged account:

1. Contributions are tax-deductible.

2. Growth is tax-free.

3. Withdrawals for medical expenses are tax-free.

If you are generally healthy and can afford to pay the deductible if an emergency strikes, the tax savings of an HSA often outweigh the higher deductible risk. However, this requires discipline—you must actually fund the HSA.

The “Sleep at Night” Factor: Financial Psychology

Math is logical; humans are emotional. You can run break-even calculations all day, but if a high deductible keeps you up at night, it’s not the right choice. More importantly, if you don’t have the cash, it’s a dangerous gamble.

The Emergency Fund Requirement

Here is the most sobering statistic of all: According to Bankrate’s 2024 Annual Emergency Savings Report, 56% of Americans could not pay a $1,000 emergency bill from savings.

The Golden Rule of Deductibles: Never raise your deductible to an amount exceeding your liquid cash savings.

If you raise your auto deductible to $1,000 to save $20 month, but you only have $200 in the bank, you are one fender bender away from financial disaster. In that scenario, the higher premium is the “cost of being poor”—a fee you pay for liquidity protection.

FAQ: Common Deductible Dilemmas

Does raising my deductible from $500 to $1,000 really save money?

Yes. Industry data suggests savings between 15% and 30% on the collision and comprehensive portion of your premium. However, the exact amount depends on your location, driving record, and vehicle type. Use the calculator above to check your specific break-even point.

What is a disappearing deductible?

A “disappearing” or “vanishing” deductible is a policy feature where the insurer lowers your deductible (e.g., by $100) for every year you go claim-free. It rewards safe driving but often comes with a slightly higher initial premium.

Is a $2,500 homeowners deductible too high?

Not anymore. In 2025, $2,500 is becoming a standard recommendation for homeowners with adequate emergency savings. Since home claims are rare (every 9-10 years), the cumulative premium savings over a decade usually justify the higher deductible.

Can I negotiate my deductible after an accident?

No. Your deductible is a contractual term agreed upon when you purchased the policy. You cannot change it retroactively after a loss occurs. This is why setting it correctly before an accident is crucial.

Conclusion: The “Traffic Light” Decision Matrix

The days of low premiums and $250 deductibles are largely behind us. Inflation has changed the landscape of risk. However, blindly raising your deductible to chase savings is reckless if you aren’t prepared.

Use this traffic light matrix to make your final decision:

GREEN LIGHT: Raise It

Conditions:

- You have a fully funded emergency fund (3-6 months expenses).

- The break-even period is under 3 years.

- You have been claim-free for 3+ years.

Action: Increase Auto to $1,000+ and Home to $2,500+.

YELLOW LIGHT: Hold

Conditions:

- You have some savings, but not enough to comfortably cover a double disaster (e.g., car crash and roof leak same month).

- Break-even is 3-5 years.

Action: Maintain current levels, or increase slowly (e.g., $500 to $750).

RED LIGHT: Lower It

Conditions:

- You have less than $1,000 in liquid savings.

- You live in an extremely high-risk area (bad traffic, high crime) where claims are likely.

Action: Keep the deductible low. Prioritize building your emergency fund immediately.

Ultimately, insurance is about peace of mind. If raising your deductible saves you $300 a year but causes you $3,000 worth of stress, it’s not worth it. But if you have the savings and the discipline, taking on a little more risk is the smartest way to beat the 2025 inflation surge.