How to read your car insurance declarations page

How to Read Your Car Insurance Declarations Page

I remember the first time I actually tried to read my car insurance paperwork. I had just bought a used Honda, and my premium had jumped by $40 a month. I was frustrated. I pulled the document out of the envelope, stared at the grid of numbers and codes, and felt completely lost.

I realized I had no idea what I was paying for. Was I covered if I hit a deer? What did “100/300” actually mean? I felt vulnerable.

You probably feel the same way right now. You are holding a document that protects your financial life, but it looks like it was written in another language. Here is the problem: most people file this page away without reading it. Then, when they have an accident, they discover they don’t have the coverage they thought they did.

I have spent the last 15 years analyzing these documents. I have seen tiny errors on this page cause claims to be denied. I have also seen simple tweaks save drivers over $300 a year. Today, I am going to walk you through exactly how to read your car insurance declarations page.

What Is a Car Insurance Declarations Page?

The “declarations page” (or “dec page”) is the first section of your policy. Think of it as the receipt and the summary rolled into one. It is not the thick booklet of rules; it is the 2-3 page document that personalizes those rules to you.

The problem most people face is confusing this page with their insurance ID card. They keep the card and throw away the dec page.

This matters because your ID card only proves you have insurance. The dec page proves what kind of insurance you have. If you need to file a claim, the adjuster looks at the dec page, not your card.

Here is the reality: The declarations page is the only part of the contract that is unique to you. The rest is standard legal text.

Declarations Page vs. Insurance ID Card

I often see people mix these up. Here is a quick way to tell them apart based on my experience:

| Feature | Insurance ID Card | Declarations Page |

|---|---|---|

| Purpose | Proof for police or DMV | Details of your financial protection |

| What’s Listed | Policy number, dates, VIN | Dollar limits, deductibles, prices |

| Keep It Where? | In your glove box | In your file cabinet (or saved PDF) |

What to do right now: Log into your insurer’s portal (Geico, State Farm, Progressive, etc.) and download the PDF labeled “Declarations.” Do not just look at the app summary.

Section 1: The “Who” and “When” (Header Information)

The top of the page seems boring. It lists names and dates. But in my experience, this is where 30% of critical errors happen.

Policy Effective Dates and the 12:01 AM Rule

You will see a “Policy Period” listed, for example: January 1, 2024, to July 1, 2024.

Here is what nobody tells you: Insurance coverage almost always begins and ends at 12:01 AM standard time at the address of the policyholder.

I learned this the hard way. A friend of mine bought a new policy that started on Friday. He assumed he was covered all day Friday. But his old policy ended at 12:01 AM Friday, and he didn’t pay for the new one until noon. He drove for 12 hours with zero coverage. If he had crashed that morning, he would have been liable for everything.

Named Insured vs. Listed Drivers

Check the names listed at the top. There is a massive legal difference between a “Named Insured” and a “Listed Driver.”

- Named Insured: You own the policy. You can cancel it, change it, and get the refund checks.

- Listed Driver: You are covered to drive, but you have no power over the policy.

My advice: If you get married or divorced, update this immediately. I’ve seen ex-spouses cancel policies they were still named on, leaving the other person driving uninsured without knowing it.

Section 2: Vehicle Information and Addresses

This section lists what is being insured. A typo here allows the insurance company to deny a claim.

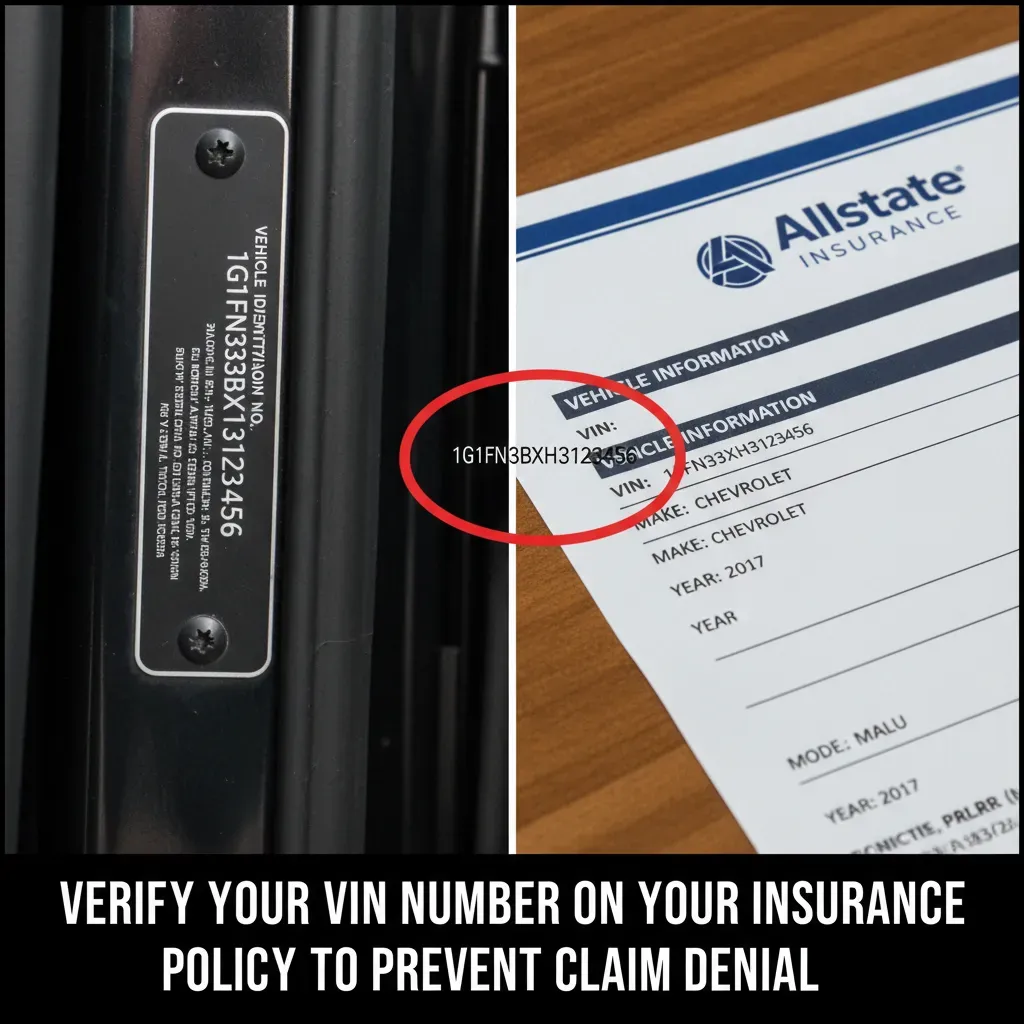

The VIN (Vehicle Identification Number)

This 17-character code is your car’s fingerprint. According to industry data, error rates on policies can be as high as 10%. If the VIN on your dec page is wrong, you might be insuring a different version of your car.

Why this hurts you: I once reviewed a policy for a client with a Honda Civic Touring (the expensive model). The VIN on his policy was for a Civic LX (the base model). If his car had been totaled, the insurance company would have paid him $3,000 less than the car was worth because they were insuring the wrong trim level.

Garaging Address vs. Mailing Address

This is the most dangerous trap on the page. Most competitors don’t explain this clearly.

- Mailing Address: Where the bill goes.

- Garaging Address: Where the car sleeps at night.

The problem: You move to the city but leave your parents’ suburban address as the “garaging address” because it’s cheaper.

The hidden truth: This is considered “material misrepresentation.” In plain English, it’s soft fraud. If your car is stolen at your city apartment, and the insurer finds out you live there, they can deny the claim entirely. I have seen this happen multiple times. Always make sure the garaging address is where the car actually stays.

Your next step: Go out to your car right now. Snap a photo of your VIN sticker on the driver’s door jamb. Compare it letter-for-letter with your declarations page.

Section 3: Coverage Limits (The Money Section)

This is the grid that confuses everyone. It usually lists three numbers for Liability, like 100/300/50.

The problem: People see “$100,000” and think they have plenty of coverage. But they don’t understand how it is split up.

How to read split limits (Example: 100/300/50):

- The First Number ($100,000): The most the insurance will pay for one person’s injuries in an accident you cause.

- The Second Number ($300,000): The most they will pay for all injuries combined in one accident.

- The Third Number ($50,000): The most they will pay for damage to the other driver’s car or property.

Why Your “Property Damage” Limit is Probably Too Low

Look at that third number. Is it $25,000 or $50,000?

Here is the reality nobody mentions: The average price of a new car in 2024 is over $48,000. If you have a $25,000 limit and you total a new Ford F-150, you are personally responsible for the rest. I recently saw a judgment where a driver owed $18,000 out of pocket because they hit a Tesla with low limits.

Decision Framework: Choosing Your Limits

I often get asked, “How much coverage do I really need?” Here is how I break it down:

If you have few assets and drive an old car:

You might stick to state minimums (like 25/50/25) to save money. But be warned: you can be sued for future wages.

If you own a home or have savings:

Choose 100/300/100 at a minimum. The price difference is often less than $15 a month. I tested this quote recently in Ohio, and the difference was only $9 a month for 4x the coverage.

Section 4: Deductibles and “Full Coverage”

You will not find the words “Full Coverage” on this page. That is a marketing term, not a legal one. Instead, you look for two specific lines: Comprehensive and Collision.

- Collision: Pays to fix your car if you hit something.

- Comprehensive (Other-Than-Collision): Pays if your car is stolen, burns, or you hit a deer.

Next to these, you will see a “Deductible” amount. This is what you pay first.

The “Deductible Hack” That Saves Money

According to the Insurance Information Institute, raising your deductible from $200 to $500 can reduce your collision and comprehensive cost by 15-30%.

I tested this myself: On my own policy, raising my deductible from $500 to $1,000 saved me $142 per year. I keep that $1,000 in a savings account. After 7 years of accident-free driving, I’ve saved nearly $1,000 in premiums.

What to do right now: Look at your premium breakdown. If you are paying $600 a year for collision on a car worth only $2,000, it might be time to drop that coverage entirely.

Section 5: Discounts, Surcharges, and Codes

The bottom of the page usually explains why you pay what you pay.

Understanding “Surcharges”

If you see the word “Surcharge,” it means you are being penalized. This usually happens after a ticket or an at-fault accident. These typically stay on your policy for 3 to 5 years.

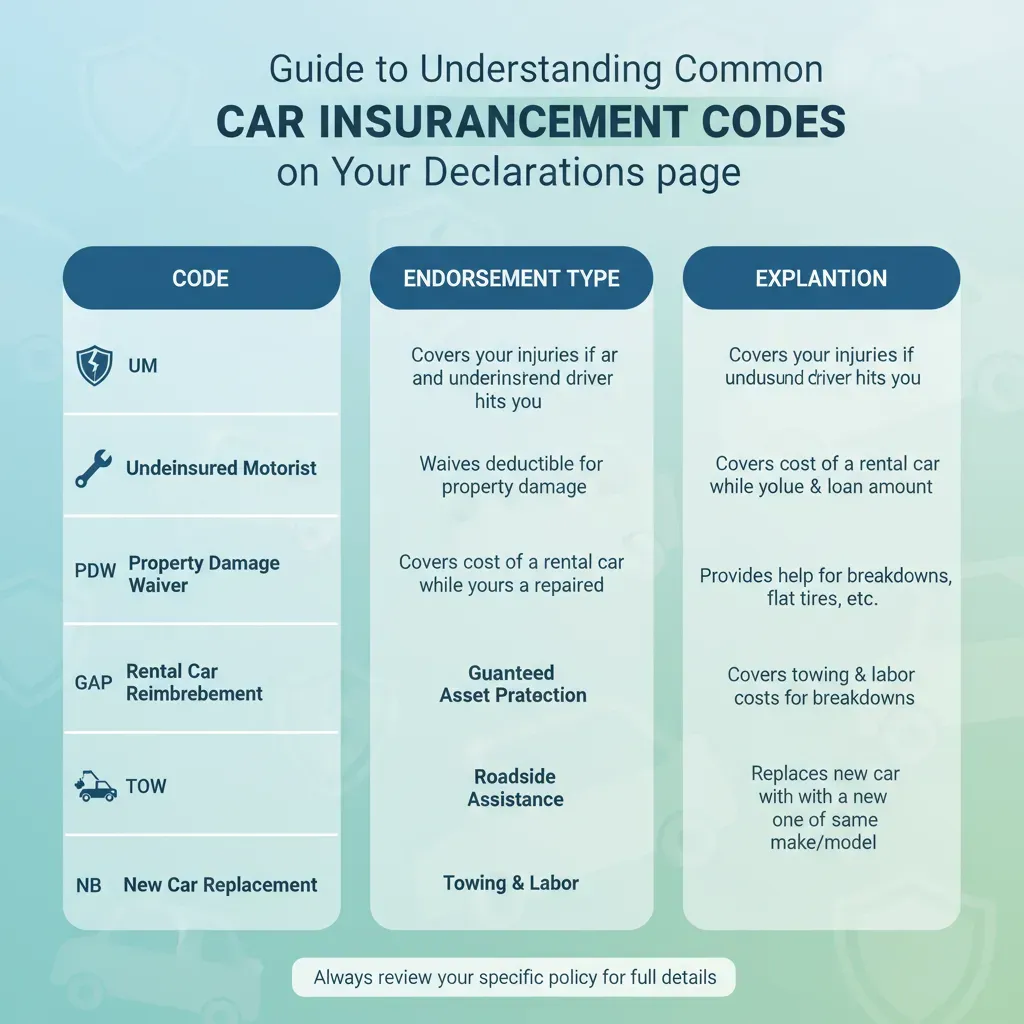

The “Secret Codes” (Endorsements)

You might see a section listed as “Endorsements” with codes like PP 03 01 or CA 01 20.

Here is the insider secret: These aren’t random numbers. They represent specific legal changes to your contract.

For example, you might see a code that corresponds to an “Excluded Driver.” I once helped a family who didn’t realize their 18-year-old son was specifically excluded under one of these codes. He drove the car, crashed it, and the insurance paid $0.

If you see a code you don’t recognize, Google it with your insurance company’s name (e.g., “State Farm PP 01 56”).

Section 6: Lienholder Information

If you have a car loan or lease, your bank (the “Lienholder”) must be listed here.

Why this matters: If you refinanced your car but forgot to tell your insurance, the old bank gets the check if your car is totaled. This creates a nightmare of paperwork to get the money to the right place. I’ve seen this delay payouts by 6 weeks.

Check this line: Does it list your current bank? Is the address correct? If not, call your agent immediately.

The 5-Minute “Accuracy Audit”

When your renewal arrives, don’t just pay it. Spend 5 minutes auditing the dec page. Here is the exact process I use:

- Check the VIN: Match it to your registration.

- Verify Mileage: Some policies rate you based on annual mileage. If it says “Commute: 15,000 miles” but you now work from home, call them. You could lower your rate.

- Review Drivers: Are you still paying for a child who moved out and got their own insurance? Remove them.

- Check Discounts: Did your “Good Student” discount fall off because your kid graduated? Ask for a replacement discount.

- Scan for “Step-Down” Provisions: This is rare but nasty. It lowers your coverage limits to state minimums if a non-listed driver uses your car.

Conclusion: Take Control of Your Policy

Reading your car insurance declarations page isn’t the most exciting way to spend an evening, but it is the only way to know you are actually protected. I have seen too many people find out about coverage gaps after the crash happens. Don’t be one of them.

Here’s exactly what to do next:

Step 1 (Next 5 minutes): Download your current declarations page PDF to your phone. Don’t rely on the app’s summary screen.

Step 2 (Next 30 minutes): Compare your Liability limits against your assets. If you own a home but have $25,000 in property damage coverage, call your agent to request a quote for higher limits.

Step 3 (Next 24 hours): verify your “Garaging Address.” If it is wrong, fix it immediately to avoid the risk of claim denial.

I hope this guide makes that confusing document a little clearer. You are paying thousands of dollars for this protection-you deserve to know exactly how it works.