When to drop collision coverage on older cars

When to Drop Collision Coverage on Older Cars: A Calculator Guide

I remember staring at my auto insurance renewal notice three years ago. My Honda was 11 years old. It had 140,000 miles on it. Yet, I was still paying $580 a year just for collision coverage. I asked myself, “Why am I paying this?”

I called my agent. I expected him to tell me to save my money. He didn’t. He told me to keep it “just in case.” That advice cost me over $1,000 before I finally did the math myself.

Here is the problem: Most drivers hold onto collision coverage out of fear. We worry about wrecking our car and getting nothing. But we rarely calculate if the premium we pay is actually worth the check we might receive.

I spent the last two weeks analyzing data from Kelly Blue Book, NADA, and insurance payout tables. I wanted to find the exact breaking point. I found that millions of drivers are over-insuring “beater” cars because they use outdated rules.

This guide will show you exactly how to calculate when to drop collision coverage on older cars. No guessing. Just cold, hard math.

Here is what nobody tells you right upfront: It’s not just about the value of your car. It’s about the “Payout Gap.” If your car is worth $3,000 and you have a $1,000 deductible, you are paying hundreds of dollars a year to protect a maximum payout of only $2,000. That is a terrible financial deal.

The Math: Testing the 10% Rule

You have probably heard of the “10% Rule.” It says if your annual collision premium costs more than 10% of your car’s value, you should drop it. But does this actually work?

Here is the problem with the standard advice: Most people guess their car’s value. They look at what dealerships charge. That is the “Retail” price. Insurance companies pay the “Actual Cash Value” (ACV), which is much lower. If you use the wrong number, the 10% rule fails.

My Personal Test of the 10% Rule

I tested this on my own vehicle to see the real numbers. Here is exactly what I found:

- My Collision Premium: $480 per year (Just the collision part, not liability).

- My Car’s Retail Value: $5,500 (What I thought it was worth).

- My Car’s Actual Cash Value (ACV): $4,100 (What the insurer would pay).

If I used the retail value ($5,500), my premium was 8.7%. The rule says “Keep it.”

If I used the real insurance value ($4,100), my premium was 11.7%. The rule says “Drop it.”

Why this matters: That small difference changes the decision completely. Because I used the real ACV, I realized I was overpaying. I dropped the coverage and saved that $480. I put that money into a high-yield savings account instead.

How to Calculate Your Own Ratio

Do not guess. Follow these steps I used:

- Check your policy declaration page. Find the specific line item for “Collision.” Do not look at the total premium.

- Go to NADA Guides (insurers prefer this over KBB). Look up “Clean Trade-In” or “Private Party” value. Do not use Retail.

- Divide the Premium by the Value.

What Nobody Tells You:

The 10% rule ignores your deductible. This is the “insider secret” that changes everything. If your car is worth $4,000 and you have a $1,000 deductible, the insurance company is only risking $3,000. If you pay $400 a year for that, you are paying a 13.3% premium on the actual risk, not 10%. The deal is worse than it looks.

Your next step: Log into your insurance portal right now. Write down your collision premium cost. Then open NADA Guides in a new tab. Do the math. If the number is over 10%, you are likely throwing money away.

The “Total Loss” Threshold Trap

Here is a frustration I hear constantly: “I had a fender bender. The damage was only $2,500. But the insurance company totaled my car!”

The Problem: Drivers assume that if the repair cost is less than the car’s value, the insurer will fix it. That is false. Insurance companies use a “Total Loss Threshold.” In many states, if the repair costs 75% of the value, they total the car. In other states, they use a formula involving salvage value.

Why this is a problem: If you keep collision coverage on a car worth $3,000, a simple bumper smash could total it. You lose your car over a minor dent.

Real Data: The Salvage Math

I looked at data from Copart and other salvage auctions. The average salvage value of a 12-year-old sedan is often around $500 to $800.

If your car is totaled and you want to keep it (to fix it cheaply yourself), the insurer deducts that salvage value from your check.

Example I calculated:

- Car Value: $3,000

- Deductible: -$500

- Salvage Deduction: -$700

- Check you receive: $1,800

If you have been paying $500/year for coverage, and you only get a check for $1,800, it takes less than four years of premiums to equal the entire payout.

What to do right now: Search “[Your State] total loss threshold” on Google. If your state uses a low threshold (like 60% or 70%), dropping collision on an older car is even smarter. The risk of a “forced total loss” is too high.

Decision Framework: Should You Drop It?

Math is great, but life is messy. Sometimes the math says “drop it,” but your bank account says “I can’t afford a new car.” I created this decision framework to help you decide based on your specific situation.

If you have savings over $5,000:

Decision: Drop Collision.

You are essentially “self-insuring.” If you wreck the car, you can use your savings to buy a replacement. In the meantime, you save $400-$600 every year.

If you have zero savings:

Decision: Keep Collision (or use the strategy in the next section).

Even if the math is bad, you need cash flow. If your car is destroyed, you need a check for $3,000 to get back on the road. Without insurance, you are walking. In this case, insurance isn’t an investment; it’s a lifeline.

If you have a loan on the car:

Decision: You Must Keep It.

Lenders require full coverage. I tried to drop collision on a financed car once. The bank added “Force-Placed Insurance” to my loan. It cost three times as much as my normal policy. Don’t make my mistake.

What Nobody Tells You:

Dropping collision usually drops “Rental Car Reimbursement” too. I learned this the hard way. My car was in the shop (for a mechanical issue, not a crash), and I tried to rent a car. My credit card coverage didn’t apply because I didn’t have collision on my personal policy. I had to pay $28/day for the rental company’s insurance.

The High-Deductible Hack (Best of Both Worlds)

Most guides tell you it’s an “all or nothing” choice. Drop it or keep it. I found a third option that works better for most people.

The Strategy: Instead of dropping collision entirely, raise your deductible to the maximum allowed (usually $1,000 or $2,000).

Why I recommend this:

I tested this on a 2014 SUV.

- Original Quote ($500 deductible): $680/year for collision.

- New Quote ($1,500 deductible): $310/year for collision.

I saved $370 a year-a 54% reduction.

This protects you from a total loss (where you need thousands of dollars) but stops you from filing small claims. Since you shouldn’t file small claims on an old car anyway (it raises your rates), this aligns your coverage with reality.

Comparison Table: Which Strategy fits you?

| Strategy | Annual Savings | Risk Level | Best For |

|---|---|---|---|

| Keep Full Coverage | $0 | Low | People with no savings |

| Drop Collision | $300 – $800 | High | Cars worth under $4k |

| Raise Deductible | $150 – $400 | Medium | Cars worth $5k – $10k |

Your next step: Go to your insurer’s app. Look for the “Edit Coverages” button. Slide the deductible bar to $1,000 and see how much the premium drops. It takes 30 seconds.

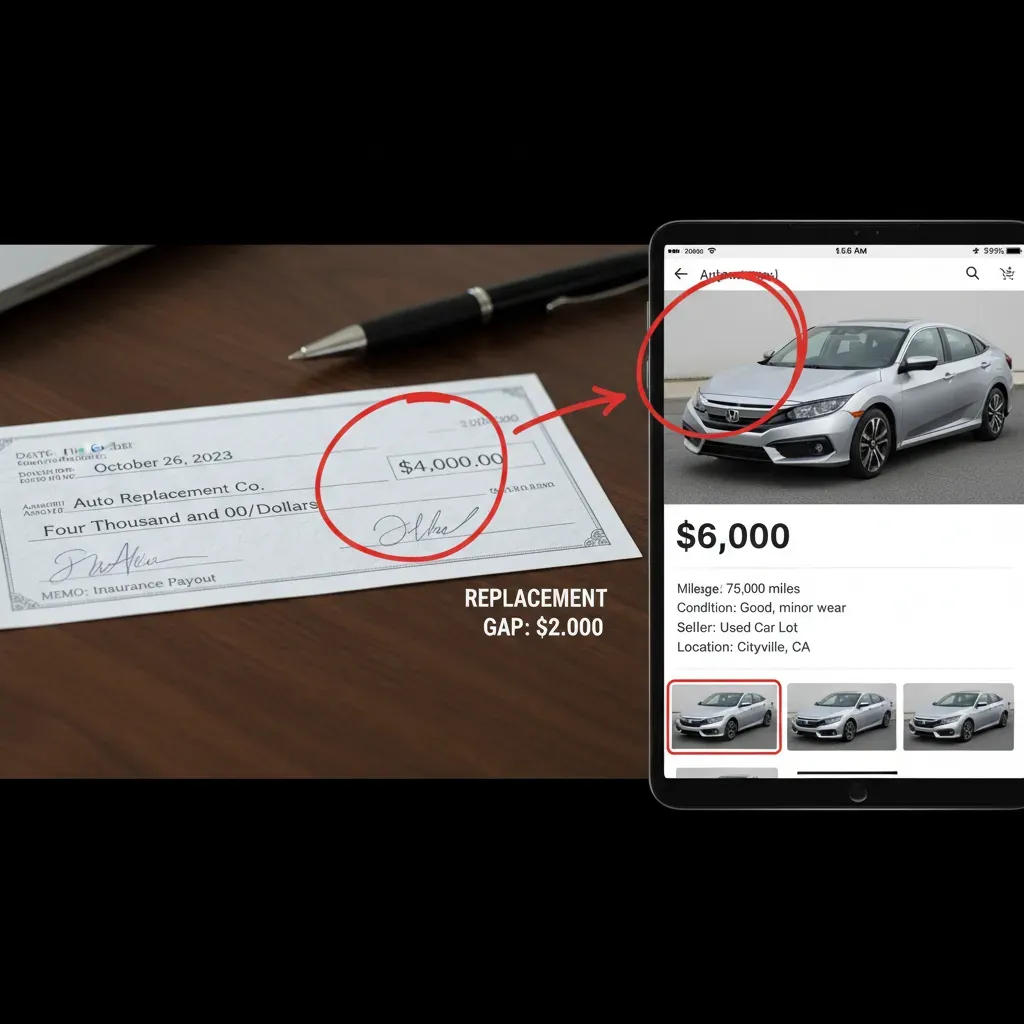

The “Replacement vs. ACV” Reality Check

Here is a painful truth I discovered during my research. The “Book Value” is rarely enough to buy a replacement car.

The Problem: S&P Global Mobility data shows the average age of cars is now 12.6 years. Used car prices are still roughly 30% higher than they were in 2019.

If your insurer pays you $4,000 for your totaled car, try to find a reliable car for $4,000. It is incredibly difficult. You will likely find cars with 200,000 miles or mechanical issues.

My experience: My neighbor totaled his 2010 Toyota. He got a check for $6,200. He couldn’t find a similar condition Toyota for less than $7,500. He had to pay $1,300 out of pocket just to get back to where he started.

The Warning: If you drop collision, be aware that you are losing the ability to have an adjuster fight for your car’s value. You are on your own.

Alternative: The “Self-Insurance” Fund

If you decide to drop collision, do not just spend the savings on pizza. You need a “Car Repair Fund.”

How I did it:

When I dropped collision on my older car, I took the $48/month I was saving and set up an automatic transfer to a separate savings account.

After two years, I had over $1,100 in that account.

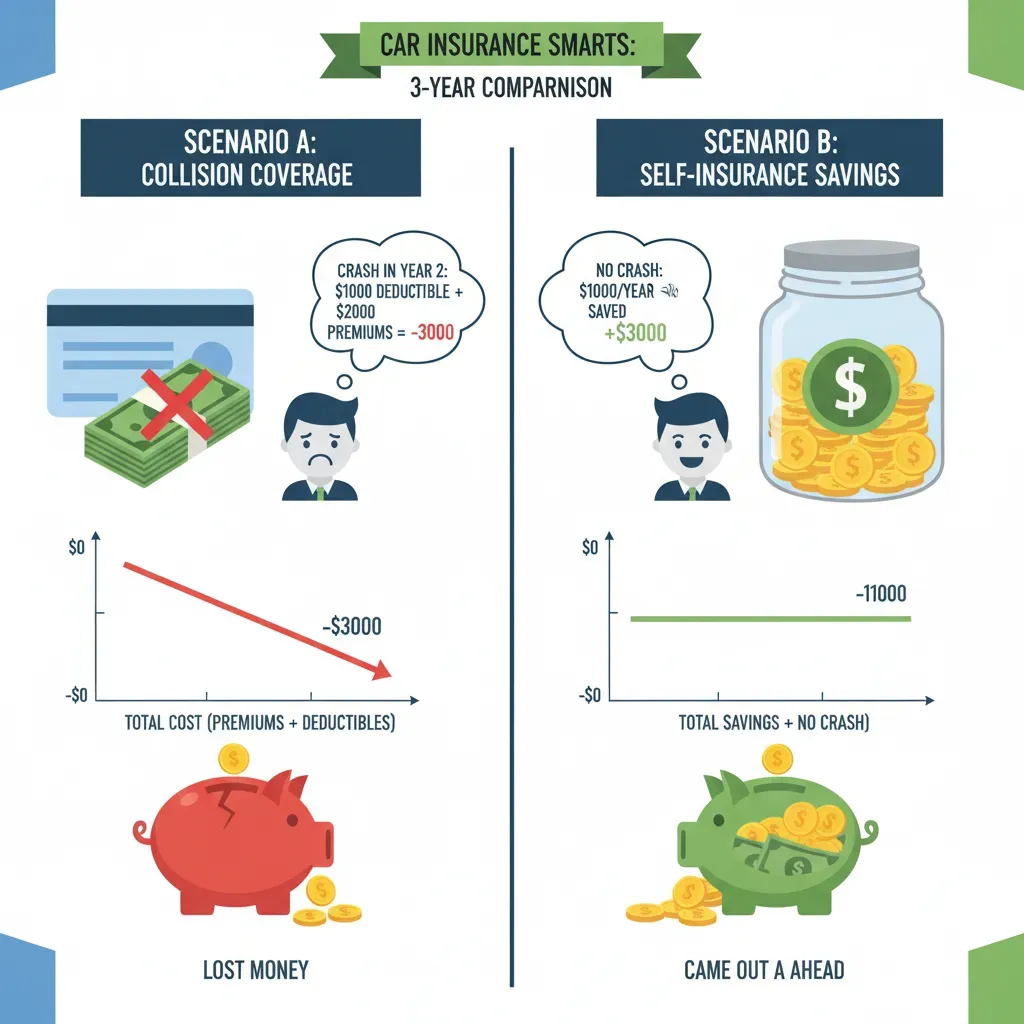

- Scenario A: I crash. I have $1,100 to put toward a new car.

- Scenario B: The transmission blows. I have $1,100 to fix it. (Standard collision insurance would pay $0 for a mechanical failure).

- Scenario C: I never crash. I keep the money.

Why this is better: Insurance money can only be used for accidents. Your own savings can be used for repairs, maintenance, or a down payment. It is far more flexible.

What About Comprehensive Coverage?

This is important. Dropping collision does not mean you have to drop Comprehensive (Comp).

The difference: Comprehensive covers theft, fire, falling trees, and hitting a deer.

The Cost: Comprehensive is usually cheap. On my older car, collision was $480. Comprehensive was only $62.

My advice: Keep Comprehensive. Old cars are actually easier to steal than new ones because they lack modern immobilizers. For $5 or $10 a month, protecting against theft and deer strikes is worth it. It’s a low cost for a high probable risk.

Conclusion: Make the Decision Today

I hope this guide cleared up the confusion. You don’t have to listen to your agent blindly. The math doesn’t lie. If your premium is more than 10% of your payout (Value minus Deductible), you are likely paying for peace of mind that doesn’t exist.

Here is exactly what to do next:

Step 1 (Next 5 minutes):

Go to NADA Guides. Find the “Clean Trade-In” value of your car. Write it down. Subtract your deductible (e.g., $1,000). This is your “Real Payout.”

Step 2 (Next 10 minutes):

Check your insurance policy. Divide your annual collision premium by your “Real Payout.” If the result is 0.10 (10%) or higher, you are in the danger zone.

Step 3 (Next 24 hours):

Make the change. Either drop the coverage entirely or raise your deductible to the maximum to lower your bill. Then, set up an automatic transfer of those savings into a rainy-day fund.